Q: How have the property tax rates changed in the past decade?

A: The short answer? Local property taxes since 2012 have increased by about 40%, outpacing the rate of inflation by nearly four times.

The long answer? Property tax increases still outpace inflation, but as with all things taxes, the answer is a little more complicated than simple addition.

Now that the budgeting season is over, you might be trying to wrap your head around a 6.27% increase in the average tax bill next year, which The Mercury reported recently. For most Manhattanites, that tax number is made up of the combined property tax increases from the city, county and school district.

When discussing the property tax, local authorities typically use the term “mills.” A mill refers to a dollar in property tax for every $1,000 in assessed, property value. Each year, the county appraiser calculates what each real estate property in the county is worth for this purpose, and by state statute, the actual taxable value of each residential property is just 11.5% of the appraised value. For a $100,000 home, that means the mill levy only applies against a $11,500, or 11.5%, value of the home. Note that this rate only applies to residential properties.

The Mercury uses a $100,000 home — even though the average value of a home in Riley County has been about double that figure recently — as a baseline for calculating the average property tax increase. That’s because an $100,000 example is easy to scale for individual readers.

For example, if your home is actually worth $270,000, simply divide that by $100,000 to get 2.7, and then multiply that amount by the printed property tax dollar increase to determine by how much your individual property taxes will change.

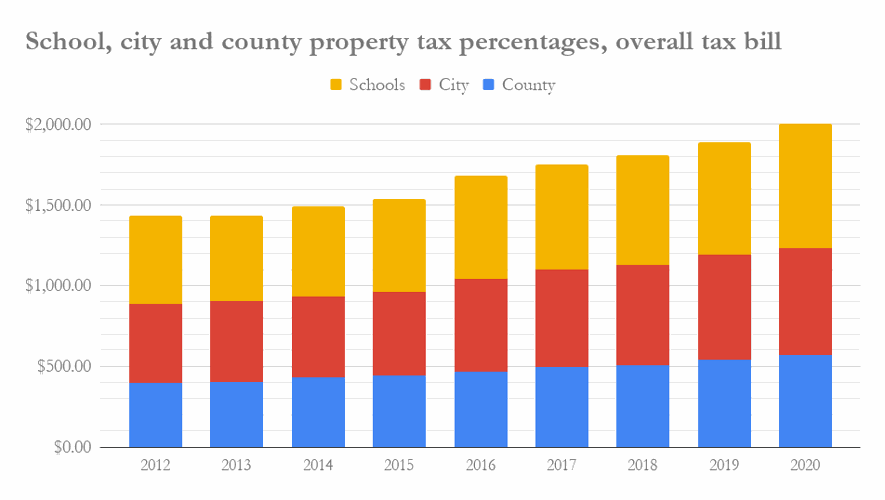

Since 2011, the school board and Manhattan and Riley County commissions have collectively voted to increase the mill levy by 26.369 mills, from 128.575 to 154.369.

In 2012, a homeowner with a house valued at $100,000 paid $1,432.61 in combined property taxes for the city, county and school district. Fast forward 8 years, and assuming that homeowner kept that same home, they will pay $2,012.93 in 2020 taxes. In essence, that homeowner will pay $580.32, or 40.51%, more than they did in 2012.

That increase is made up of two components. The first is the same logic driving the game of Manhattanopoly: people like to buy property, and with demand, the prices tend to creep up.

Real estate also tends to generally increase in value, barring a disaster or drastic change in circumstance, so each year, the county appraiser is tasked with figuring out the market value of each of the county’s real estate parcels for the very purpose of determining how much to tax each property owner.

In this specific case, the average value of a single-family home grew by 15.55% since 2011. Since each organization determines their tax rates in the summer preceding each tax year, The Mercury used 2011’s appraisal rates for the 2012 tax year and 2019’s rates for 2020. Unfortunately, the county appraiser’s office only has readily available data from 2011 onward, so these historical calculations are limited.

Using those rates, you immediately see that a homeowner’s 2012 property isn’t really worth $100,000 anymore, at least according to the county appraiser. It’s worth $115,550, or 15.55% more, so the effective property tax is also higher, even with a flat mill.

That brings us to the next component of the increase: increases in the mill levy. Generally speaking, even a flat mill will bring in more property tax revenue for the government, because as mentioned before, property tends to increase in value.

But increases in the actual mill levy will of course drive up property taxes each year, and since 2012, the school board and city and county commissions have collectively increased the mill levy rate by 26.369 mills. If you assume that house values somehow stayed flat for eight years, that mill increase accounts for a $303.24 property tax increase.

Combining the mill increases with the property value increases since 2012 results in a 40.51% increase in the average homeowner’s tax bill. These components drive The Mercury’s year-to-year tax bill calculations each summer.

However, a longer-term comparison introduces a new variable: inflation. With inflation, dollars are worth less, even if just marginally, each year (in part, because property values increase actually), so a 2012 tax dollar isn’t really worth the same as a 2020 tax dollar. In short, year-to-year calculations, inflation is usually under 3%, a negligible amount for tax calculations, so The Mercury leaves it out to keep taxes simple.

But on longer-term scales, even in just 8 years, inflation becomes a significant factor to consider, especially in comparison to the rate of property tax growth. From June 2012 to June 2019, inflation was 11.62%, according to the U.S. Department of Labor’s Consumer Price Index. As much as we’d like to know what inflation will be in 2020, the federal government has no ability to see into the future (that we know of), and the latest month for which data is available is June 2019.

With that in mind, assuming the mill levy stayed flat and property taxes increased at the rate of inflation since 2012, those $1,432.61 in taxes paid then would be $1,855.73 in 2020, once the increase in the house value is considered as well. That’s an increase of $423.12, or 29.53%, a somewhat more palatable increase for homeowners.

It’s worth noting that that 29.53% increase is the natural consequence of economic changes way beyond the jurisdiction of any local official, unless they somehow happen to be on the Federal Reserve board.

So accounting for inflation, how much have the school board members and city and county commissioners added to your tax bill since 2012? To figure that out, we just need to compare the increase due to inflation and increase in property value, and the actual amount homeowners will pay in 2020.

The math is this: that homeowner who owned a $100,000 home in 2012 will pay $2,012.93, which is $157.20 or 8.47% higher than if the mill levy had stayed flat.